The application users the Black-Scholes formula to give a theoretical estimate of the price of European-style options.

It also calculates the Greeks which measure the sensitivity of the value of a derivative or a portfolio to changes in parameter value(s) while holding the other parameters fixed. The Greeks for Black-Scholes are obtained by differentiation of the Black-Scholes formula.

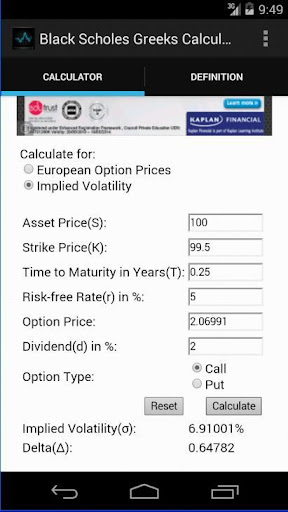

The app of Version 1.1 add a functionality to calculate the implied volatility with the bisection method. The bisection method is applicable when we wish to solve the equation f(v)=BlackScholes(S, X, T, r, d, v)-OptionPrice for the real variable v, where f is a continuous function defined on an interval [a, b] and f(a) and f(b) have opposite signs.

At each step the method divides the interval in two by computing the midpoint c = (a+b) / 2 of the interval and the value of the function f(c) at that point. Unless c is itself a root (which is very unlikely, but possible) there are now two possibilities: either f(a) and f(c) have opposite signs and bracket a root, or f(c) and f(b) have opposite signs and bracket a root. The method selects the subinterval that is a bracket as a new interval to be used in the next step. In this way the interval that contains a zero of f is reduced in width by 50% at each step. The process is continued until the interval is sufficiently small.

免費玩Black-Scholes Greeks Calc APP玩免費

免費玩Black-Scholes Greeks Calc App

Black-Scholes Greeks Calc APP LOGO

Black-Scholes Greeks Calc APP QRCode

| 熱門國家 | 系統支援 | 版本 | 費用 | APP評分 | 上架日期 | 更新日期 |

|---|---|---|---|---|---|---|

| 未知 | Android Google Play | 1.2 App下載 | 免費 | 1970-01-01 | 2015-03-11 |