Getting a loan? Compute and manipulate the numbers to your advantage.

The interest rate here has a name, it's called the APR (annual percentage rate), this reflects the real time value of money.

Many reputable lenders cheat, they use a method, which prior to 1940, was only used by loan sharks, called the rule of 78's.

The rule of 78s is different way of calculating interest in each payment. This method is called front loading. Meaning you pay more interest at the beginning of the loan than the time value of money would require. Why is this a rip-off?

Here is a thought experiment. If all the first payments are interest and you payoff the loan early, you will pay the full amount you borrowed plus interest that never accrued.

Here is an example: You borrow 10,000 and your payment is $200. Normally based on the time value of money a part of each payment is interest. At first a little over half the payment is interest ($100 approx.) declining over 7 years of the loan to the last payment where the interest component is $0. The reason that the interest cost declines is that as you make payments the amount borrowed becomes less making the interest owed less.

What if the beginning payments were all interest until all the interest was paid after which you started paying off the amount you borrowed? At the end of 3 year you have paid off all the interest now you can start paying of the loan. But what if you now paid off the loan. You would have paid $6,800 interest plus the original $10,000 loan for a total of $16,800 instead of $4,000 interest (based on the time value of money) plus the original $10.000 or $14,000. You would have paid $2,000 extra.

Now the rule of 78’s in not this extreme, but you get the idea.

Mortgage lenders who make long-term loans (20-30 years) are more up-front about it. The charge what are called points up-front, which is really just prepaid interest. Again if you pay off early, you paid too much. They count of this.

When we get married we think it will be forever. For car and house loans people change their mind every 3 to 5 years. For marriages it's a little longer. So avoid the rule of 78’s and up-front “points”. Ask for a amortizing loan based on the time value of money with 0 points.

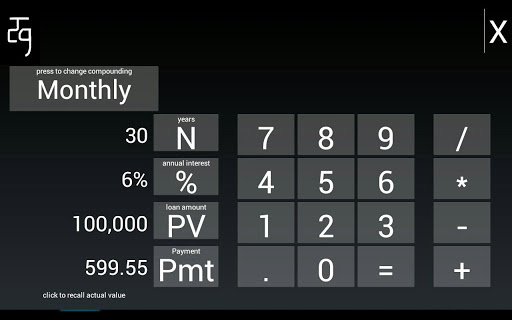

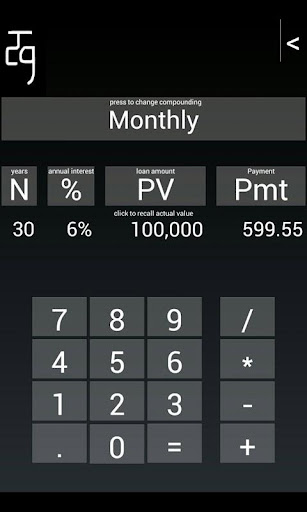

Double check what the lender tells you. What should the payment be vs. what they quote? What is wrong with their numbers? Let see what they are really doing. Enter the length of the loan, interest rate, and loan amount and compute what the payment should be. Put in their payment, press % to see what interest they are really charging you. This is powerful tool for manipulating the numbers to your advantage.

Buy a house.

PV = 300,000

% = 3.75

N = 30 years

Press Pmt - to see the required monthly payment.

But what if you want a lower payment?

Enter the new payment (Pmt)

Press % - to see the required interest

or

Press N - to see the see the required years

What if you want to make the payments yearly, press the "Monthly" button several times to get to "Yearly", the payment will recalculate.

The interest rate (%) and years on loan (N) are always yearly/annual numbers.

The Pmt is Yearly, Monthly etc. Depending on the setting.

About the author: Having been a real estate broker for 40 years. I have seen all sorts of slimy lending practices. Armed with a tool like this is your best defense again getting robbed.

免費玩FinCalc APP玩免費

免費玩FinCalc App

FinCalc APP LOGO

FinCalc APP QRCode

| 熱門國家 | 系統支援 | 版本 | 費用 | APP評分 | 上架日期 | 更新日期 |

|---|---|---|---|---|---|---|

| 未知 | Android Google Play | 1 App下載 | USD$0.99 | 1970-01-01 | 2015-01-14 |